Introduction: Nonprofit organizations are growing in impact globally. Growth can accompany additional access to resources, funding, and governmental provisions. Contrasting how organizations are structured and function financially in prominent countries can help citizens and policymakers identify flaws and strengths in existing systems to better inform financial decisions. Nonprofit systems in South Africa and the US will be detailed in this paper. Specifically, the principles which inform perceptions of nonprofits, the national legal and individual administrative structures of nonprofits will be outlined. Detailing the ways in which nonprofits are held financially accountable by national governments is crucial to nonprofit system analysis.

United States (US) Nonprofit Principles and Ideology: In the US, the tax-exempt status is founded on the principle that nonprofits are providing a public or social good which is the responsibility of the government. It would be counterproductive for the government to tax its own organizations, as taxes are collected in part to provide public goods, therefore, the tax-exempt category of the IRS Section 501(c) code was established (McLaughlin 2016). Additionally, the United States approaches nonprofits like a corporate structure. The management and corporate structure of for-profit organizations apply to nonprofits because corporations are viewed as “distinct entities like individual people, and corporations have their own collection of responsibilities, liabilities, and powers,” which can also be utilized for nonprofit accountability as well (McLaughlin 2016, p.4).

US legal structure of nonprofits: Corporate structures are diverse and depend on the type of business; nonprofits are similar in diversity so they can find and utilize a corporate structure that fits them best. To choose the best organizational structure, a nonprofit must first determine its functions and what it aims to be. To establish a nonprofit, a state must incorporate the organization based on state-specific guidelines and regulations. Incorporation is crucial for nonprofits filing for tax-exempt status as the federal Internal Revenue Service (IRS) only offers an exemption for recognized trusts, corporations, or associations which are all registered at the state level (IRS 2019, p. 20). IRS Section 501(c) includes all types of organizations that provide public or welfare goods and operate on the objective of providing a service rather than earning a profit (IRS 2019, p. 20).

The 501(c) code entails many things for an organization; all organizations under this category are exempt from federal and usually state corporate taxes, and private foundations are not included (McLaughlin 2016, p. 9). A distinguishing legal attribute of nonprofits is that most of them fall under subsection 501(c)(3) corporations which include certain benefits. Section 501(c)(3) offers tax exemption from all federal, and sometimes state, taxes which can be a significant incentive for organizations, therefore the IRS identifies certain purposes that organizations must serve to be considered for that status.[1]Additionally, 501(c)(3) nonprofits receive the right to offer tax deductions to donors from their federal income taxes based on the amount they contribute to nonprofits (McLaughlin 2016, p. 9; IRS 2019, p.22).

Organizations must fill out Form 1023 or Form 1023-EZ for recognition of tax exemption under Section 501(c)(3), which entails three specific requirements. First, organizations must show they were created for and will operate exclusively to fulfill, one the purposes outlined by the IRS mentioned previously. Second, an essential rule for organizations achieving tax-exemption is that any profit earned cannot go to an individual in the staff or board of directors. People working for the nonprofit can be paid, of course, however, there cannot be direct dividends of total funds to shareholders or directors as is common in other for-profit corporations (UpCounsel, 2019). Third, Form 1023 specifically mentions that a nonprofit organization “won’t be organized or operated for the benefit of private interests, such as the creator or the creator’s family, etc.” (IRS 2019, p. 23). Nonprofits are limited on their influence over politics via propaganda, lobbying or other legislative activity; which can only make up 10 to 20 percent of the organization’s total activities (UpCounsel, 2019). Aside from certain lobbying expenditures approved by the IRS, a nonprofit cannot attempt to influence legislation directly (IRS 2019, p. 23). Finally, if a nonprofit is shut down, its assets cannot be given to any individuals they must be donated to the government in charitable contributions.

The focus of this paper is charitable organizations which fall under 501(c)(3) rules and tax status. The IRS has further identified that charities must operate for purposes beneficial to the public interest, some examples of this type of organization include;

“…relief of the poor, the distressed, or the underprivileged; advancement of religion, advancement of education or science; erection or maintenance of public buildings, monuments, or works, lessening the burdens of government, lessening of neighborhood tensions, elimination of prejudice and discrimination, defense of human and civil rights secured by law; and combating community deterioration and juvenile delinquency” (IRS 2019, p. 28).

There are nearly one million 501(c)(3) charities in the United States which receive funding from the government, public donors, and corporations (UpCounsel, 2019). Financial accountability of such a large tax-exempt sector is crucial.

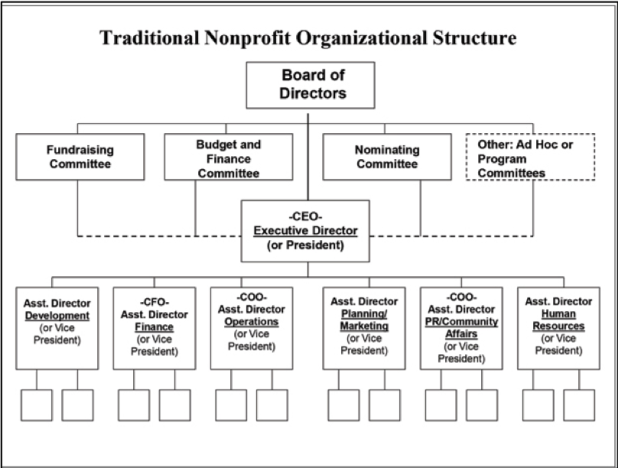

US Organizational structure of individual nonprofits; General organization for nonprofits includes a Board of Directors who serve as the governing body focusing on an organization’s mission, strategy and goals, and staff members who serve as the functioning arm responsible for implementing the organization’s day to day duties and carrying out programs (Zerwin, 2009). An Executive Director (ED) is hired by the Board and responsible for monitoring the working arm of the organization, including hiring and supervision of all staff members (Zerwin 2009, p. 18). Larger nonprofits have several functioning arms to implement nonprofit programs, for example; a charity may have a development, operations, public relations, or human resources arm, each led by Assistant Directors who report to the Executive Director. In larger nonprofits, the Board of Directors usually splits into committees overseeing budget and finance, fundraising, nominations, and other ad hoc activities or programs[Picture Below](Zerwin 2009, p. 18).

How organizations function financially in the US: The financial accountability and responsibility of a nonprofit fall on the Board of Directors[3](Zerwin 2009, p. 20). Nonprofits create a budget to have a game plan for how to fulfill their mission at a given point in time; usually at the beginning of the nonprofit’s operating year (Zerwin 2009, p. 3). An operating budget has income and expense information or contains information for day-to-day functions of a nonprofit. Operating budgets can be “line item, which project and control income by source and expense by object, or a “program budget,” which uses line item but also controls income by the purpose for which it is received and expense by the purpose for which it is spent” (Zerwin 2009, p. 25). An effective budget has an introductory narrative, explanations of important line items, presentation of past, current, and proposed income and expense, and a month-by-month cash flow projection which are all necessary components to present the budget to the Board for approval. The goal of a budget is to balance between income and expense.

A statement of cash flow reports a nonprofit’s change in its cash from operating, investing, and financing activities during the accounting period (Zerwin, 2009). The monthly income of a nonprofit varies while expenses remain the same because income or revenue, in this case, is how much donors contribute monthly, which alters. Monthly discrepancies require nonprofits to be vigilant in ensuring there are financial reserves present for months during which an organization might have to run on a deficit, meaning there are more expenses than revenues. Usually, most nonprofits aim for a financial reserve of 25% of expected annual operating costs to fill gaps in expenses during deficit months (Zerwin 2009, p. 38). After the initial projection, the budget is amended monthly and by the end of the year, after audits and other analyses, the Board of Directors approve the budget.

US Nonprofit financial accountability mechanisms and forms; A nonprofit can be held financially accountable through multiple documents. The Statement of Activities is an active document stat allows nonprofit staff members to analyze the organization’s financial health and see if the operating budget is running in a surplus or a deficit. (Zerwin 2009, p. 42). The Statement of Financial Position shows a static image of the organization’s overall financial health, namely an organization’s assets, liabilities, and net assets at a specific point in time (Zerwin 2009, p. 42). The Statement of Financial Position gets approved at the end of the year by the Board of Directors and must be audited by an independent auditor if the nonprofit handles annual budgets of $500,000 or more (IRS, 2019). While smaller nonprofits are not legally required to have independent audits, it is often seen as a necessary investment to assure transparency. The Annual Report is a publication for major donors most large nonprofits create summarizing annual program activity, a full financial report, and a list of Board and staff members involved (Zerwin 2009, p.50). The most important financial accountability mechanism is the IRS Form 990 all 501(c)(3) nonprofits must fill out (IRS, 2019). Form 990 provides a comprehensive view of a nonprofit as it requires essential financial information for wages, programs, and all nonprofit activities in a year.[PictureBelow] Form 990 is a way for IRS to ensure the tax-exempt status has not been violated, and for the public to assess a nonprofit before making charitable contributions.

South Africa (SA) Nonprofit Principle and Ideology: After Apartheid and the formation of a new South African Republic, the Nonprofit Organizations Act (NPO Act) was ratified replacing the restrictive Fundraising Act of 1978 (Wyngaard,2019). South African nonprofits are based on the principle of “ubuntu” of the Nguni language translating directly to “humanness;”

“Ubuntu… is often illustrated by the idiomatic expression umuntu ngumuntu ngabantu (a person is a person because of people). Ubuntu implies a relationship of mutual and reciprocal responsibility between individuals and communities” (Rosenthal, 2012, p.4).

Ubuntu creates the foundation of values that nonprofits must follow, and these values are further explicitly detailed in the three main pieces of legislation regarding SA nonprofit structures; Nonprofit Organizations Act, Trust Property Control Act, and the Companies Act (Fodor and Radebe,2018). Legally, nonprofits are categorized under the heading of “welfare” handled by local and national government. Therefore, SA nonprofits must adhere to federal and provincial rules and categories (Fodor and Radebe,2018).

South Africa Nonprofit Legal Structure: Non-Profit Organizations (NPOs) in South Africa are created under three major categories. First, Voluntary associations established under common law can be registered under the NPO Act, however, it is not obligatory for these organizations to be registered at all. Second, Nonprofit Trusts established under statutory law, registered according to the Trust Property Control Act of 1988. Third, Nonprofit companies incorporated for a public benefit objective, similar to US nonprofits, and registered under the Companies Act. (Fodor and Radebe,2018;Liu 2018, p. 2).

Once an organization has determined what type of NPO they are, there are four additional legislative tiers they have access to. First, there is a national voluntary registration status which ensures certain governance criteria is met, and non-profits cannot distribute profits to members (Liu, 2018). Second, are partial tax exemptions, for which NPOs must apply for “public benefit organization” (PBO) status to receive (Liu, 2018). PBO status can only be granted if an organization’s sole purpose is to undertake one or more public benefit activities carried out in a not for profit altruistic manner, and if resources of the organization are not used to directly or indirectly support, advance, or oppose any political parties (this does not exclude lobbying) (Republic of South Africa, 2009). PBOs receive many fiscal benefits including partial tax exemption, exemption on donations tax, and for some organizations, exemption from transfer duty on immovable property (or trust deeds) (Liu 2018, p. 2). PBOs can fall under voluntary NPOs, trusts, or companies as long as they pursue public benefit activities relating to “welfare and humanitarian, healthcare, education, religion, and conservation” (Fodor and Radebe,2018). Third, is donor deductibility status, which allows the organization to receive tax-deductible donor contributions (Republic of South Africa, 2009). Fourth, some organizations can receive Value Added Tax or Income Tax Act incentives which limit taxes on goods consumed by the organization (Republic of South Africa, 2009).

Voluntary organizations are unique in South Africa as they have no office of registry yet, these are the most common forms of NPOs within South Africa (Radebe, 2018). Voluntary organizations only require three or more people to, orally or in writing, agree to achieve a common objective which is primarily not for profit; usually, these agreements are made by drafting a constitution for the NPO (Radebe, 2018). Voluntary associations which are a result of the common law and unregulated by any statues are known as universitas, while bodies that remain unincorporated at common law are known as non-corporate associations (Liu 2018, p. 3). The legal provision of a universitasis mandated by courts based on certain requirements; the organization is identified as an entity notwithstanding a change in membership, the organization is able to hold property distinct from its members, and no members of the organization own rights to the property of the association (Liu 2018, p. 3). Voluntary organizations are easy to establish and are favored by smaller community based nonprofit organizations because they have limited incomes and activities. Community-based nonprofits often used voluntary organizations to work locally and find small bottom-up projects rather successful (Wyngaard, 2019; Matthews, 2017). However, outside South Africa, such organizations are viewed skeptically and the structure is deemed unsuitable for large nonprofits due to broader accountability and transparency issues (Fodor and Radebe, 2018).

Trusts are based on a deed registered with the Master of the High Court in the physical jurisdiction of an organization (Liu, 2018). Not for profit trusts must also appeal to the Income Tax Act requirements to receive tax deductions. There are many pros and cons of nonprofit trusts. If a nonprofit does not meet Income Tax Act qualifications, they may have a higher liability due to the trust status than perceived (Wyngaard, 2019). Additionally, donors prefer the corporate structure for transparency measures (Radebe, 2018). At the same time, trusts are more flexible legal structures which can be used for a variety of nonprofits, and the formation of trusts is less complex and costly than nonprofit company structures (Wyngaard, 2019).

Nonprofit companies are recognized when an organization has three or more identified directors who take full responsibility for the organization, the organization fulfills a public benefit objective outlined in the Companies Act Schedule I [5], and the organization does not distribute income or property to members (Liu 2018, p. 3).

South Africa Organizational Structure of Individual Nonprofits; Most SA nonprofits have similar structures to US nonprofits, with a governing board of some sort, a “CEO” or ED, and “activity” arms, like project arms in the US, which operate day to day duties. South African international nonprofit companies are required to hire a public officer who must be in South Africa to interact with the Receiver of the Revenue and hire a South African resident representative for said company. (Fodor and Radebe, 2018).

South Africa nonprofit financial accountability Forms and Requirements: Nonprofit companies file annual tax returns under the Companies and Intellectual Property Commission (CIPC). There is a provision in Chapter three of CIPC which requires a company secretary and auditor to be appointed for accountability measures, however, the founders of an organization have a choice to comply to that measure when initially registering the organization. PBOs must provide annual financial statements to the SARS Receiver. If an organization has donor deductibility status, 18A tax exemption certificates must be issued for qualifying donations and a register of these donations must be kept (Fodor and Radebe, 2018). PBOs must send out 18A tax exemption certificates to all their donors requesting tax exemption from income for charitable contributions. Trusts do not have specific financial requirements past the trust deed; however, an annual financial statement is collected for accountability. Unregistered voluntary associations obviously have no financial forms or requirements to submit, contributing to more transparency issues. All registered voluntary associations must complete annual financial statements and report to the Directorate for NPOs created under the NPO Act.

In terms of tax deductions; PBOs can only provide deductions to donors on a limited 10% of annual income in a fiscal year, any donations more than that will be taxed, a donor can only collect tax deductions with a receipt from the nonprofit which is a Form 18A donor certificate. For tax exemption approval, all funding from a donor must go towards one of the five categories of public benefit activities approved under Part II of Schedule Nine in the Income Tax Act previously listed (Republic of South Africa, 2009). Value Added Tax (VAT) Act applies to a larger amount of organizations as it is eligible for “associations not for gain,” referring to social organizations, and “welfare organizations.”[6] Many organizations can benefit from VAT due to its broad categories (Liu 2018, p.10).

US nonprofit conclusion; Overall, the US nonprofit status is based upon the principle of an organization providing public goods and services usually fulfilled by the government, allowing tax exemption on the operations of that organization. National tax-exempt organizations follow Section 501(c) IRS provisions with charities falling under the 501(c)(3) subsection allowing certain specific tax incentives. At an organization level, nonprofits have a governing and functioning arm. Financially, a nonprofit’s revenue, expenses, assets, liabilities, and net assets are essential measures for evaluating financial accountability and operations. The IRS requires financial accountability through Form 990 and external auditors. Nonprofits ensure financial accountability through; budgetary projections conducted at the beginning of the year, Statement of Activities and Financial Positions, and submission of Form 990. Donors and the public hold nonprofits accountable by requesting to view their Form 990 or an Annual Report.

South Africa Nonprofits Conclusion: South African nonprofits follow the principle of ubuntu and believe in the interconnected human relationship of helping each other. Nonprofits are categorized under; voluntary associations, trusts, and companies; each of these categories has varying federal statutes governing it. SA nonprofits can apply for; PBO status which means they are tax exempt under certain guidelines, Income Tax Exemption status to grant donors tax deductions, and VAT exemption status for international companies and foreign donations. PBOs, Income Tax, and certain VAT exemptions are only given to organizations fulfilling recognized public services or welfare services. Financial requirements and forms mandated by the national government depend on the nonprofit type.

Conclusion: The US and SA nonprofit systems are similar, in part due to the new liberalization of the South African Republic allowing NGO and tax policies to be redrafted in 2009. Each system has strengths and weaknesses. South African localized voluntary NPO structures might prove useful in other nations while eliminating certain issues. Community-based organizations are preferred by South Africans because no tax exemptions are being used, and since Apartheid, neoliberal institutions like the IMF are influencing SA nonprofits to find quick technical solutions to inequalities rather than addressing deeper foundational roots leading to inequalities, which community-led organizations do well (Matthews, 2017). VAT exemptions need policy changes as there have been cases of organizations taking advantage of this provision (Liu, 2018). SA’s PBO application system has been criticized for being too convoluted by nonprofit leaders (Rosenthal, 2012). Similarly, the US structure has been criticized for providing too many subsidies and incentives to extremely wealthy donors and is often seen as too intricate as well (Adema, 2001; Soskice, 2007). Both the US and SA are influential nations within their regions, leading the way for nonprofit systems in other nations.

BIBLIOGRAPHY

Adema, W. (2001), ‘Net Social Expenditure’ 2nd Edition, OECD, Labour Market and Social Policy Occasional Papers, no. 52. Honey, M. (n.d.). Legal Structures commonly used by Non-Profit Organisations. Retrieved from ETU: https://www.etu.org.za/toolbox/docs /building/lrc.html#similarities. Hurwit&Associates. (2019). Traditional Nonprofit Organizational Structure. Retrieved from Hurwit&Associates: https://www.hurwitassociates.com/nonprofit-organizational-charts/traditional-nonprofit-organizational-structure. Liu, L. (2018, July). South Africa.Retrieved from Council of Foundations: https://www.cof.org/sites/default/files/South_Africa-201807.pdf Matthews, S. (2017, April 25). The role of NGOs in Africa: are they a force for good? . Retrieved from The Conversation: http://theconversation.com/the-role-of-ngos-in-africa-are-they-a-force-for-good-76227 Radebe, S. F. (2018, July 1). Charitable organisations in South Africa: overview.Retrieved from Thomson Reuters Practical Law: https://uk.practicallaw.thomsonreuters.com/9-632-4485?transitionType=Default&contextData=(sc.Default)&firstPage=true&comp=pluk&bhcp=1#co_pageContainer Republic of South Africa. The Presidency. (2009). Government Gazette: Companies Act, 2008 (Report No. 32121). Cape Town: Republic of South Africa. Rosenthal, R. (2012). The Independent Code of Governance for Non-Profit Organizations in South Africa.Cape Town: Published by the Working Group on The Independent Code of Governance for Non-profit Organisations in South Africa. Soskice, D. (2010), ‘American Exceptionalism and Comparative Political Economy’, in C. Brown, B. Eichengreen and M. Reich (eds.), Labor in the Era of Globalization, Cambridge: Cambridge University Press, pp. 51-93. Ted Zerwin, Managing and Raising Money that is Not Your Own: Financial Management and Fundraising in Non-Profit Organizations, Vandeplas Publishing. Thomas A. McLaughlin, Streetsmart Financial Basics for Nonprofit Managers, Fourth Addition, John Wiley & Sons, Inc. upcounsel. (2019). Types of Nonprofits: Everything You Need to Know . Retrieved from upcounsel: https://www.upcounsel.com/types-of-nonprofits U.S. Department of the Treasury. Internal Revenue Service. (2019). Publication 557: Tax-Exempt Status for Your Organization (Cat. No. 46573C). Retrieved from: https://www.irs.gov/pub/irs-pdf/p557.pdf. U.S. Department of the Treasury. Internal Revenue Service. (2018). Publication 557: Instructions for Form 990 Return of Organization Exempt From Income Tax (Cat. No. 11283J). Retrieved from: https://www.irs.gov/pub/irs-pdf/i990.pdf. Wyngaard, R. (2019, March 6). Civic Freedom Monitor: South Africa . Retrieved from International Center for Not-for-Profit Law: http://www.icnl.org/research/monitor/southafrica.html#top

[1]According to the IRS (2019), “An organization may qualify for exemption from federal income tax if it is organized and operated exclusively for one or more of the following purposes; religious, charitable, scientific, testing for public safety, literary, educational, fostering national or international amateur sports competition…, [and] the prevention of cruelty to children or animals. To qualify, the organization must be organized as a corporation (including a limited liability company), unincorporated association, or trust” (IRS, 2019 Chapter 3, Section 501(c)(3) Organizations. Page 21).

[2]See Appendix A: Traditional Nonprofit Organizational Structure (Hurwit&Associates, 2019)

[3]The Board of Directors usually; “determines the direction for the organization, guards its mission, sets the standards and ethical guidelines, monitors its performance, and ensures the organization is managed in a responsible manner” (Flynn 2019).

[4]Form 990 includes; “income, expenses, assets, liabilities, and net assets; program, management, and fundraising expenses; amount of fund spent on lobbying; a list of Executive and higher level salaries; a listing of donors and granting institutions contributing more than $5,000,” and many other pieces of information regarding an organization’s annual performance (Zerwin 2009, p. 52).

[5]See Appendix B: Nonprofit provisions Companies Act (Republic of South Africa, 2009, p. 46).

[6]“…referring to activity under the categories of welfare and humanitarian, healthcare, land and housing, education and development, and conservation, environment and animal welfare” (Government Notice no. 112 in Government Gazette no. 27235, published 11 February 2005).